The traditional credit card market has long dominated consumer financing, but the rise of Buy Now, Pay Later (BNPL) services is reshaping this domain. With millions of consumers opting for BNPL, financial behaviors are evolving, posing both opportunities and challenges for credit card issuers and analytics-driven companies. Understanding BNPL’s impact on the payment ecosystem and addressing challenges like risk management and payment defaults is critical for stakeholders.

What is BNPL?

The Buy Now, Pay Later (BNPL) model is transforming the payments landscape by giving consumers the flexibility to purchase goods and services and pay for them over time. Unlike traditional credit cards, BNPL services allow consumers to split their payments into installments, often without interest if the payments are made on time. This payment method is rapidly gaining popularity, especially among younger consumers who prefer flexible payment options.

BNPL originated as an alternative to credit cards, particularly in e-commerce, but has now become a mainstream payment option at many online and in-store retailers.

BNPL services enable customers to make purchases and pay for them in equal installments over a set period, usually ranging from a few weeks to several months. Customers often pay no interest if they meet the payment deadlines. Merchants benefit from increased sales, and consumers enjoy the flexibility of spreading out payments without the burden of high interest rates.

BNPL market overview

As of 2023 estimates, BNPL solutions have grown significantly, with a global market size of $378.3 billion and projected to increase by nearly $450 billion between 2021 and 2026.

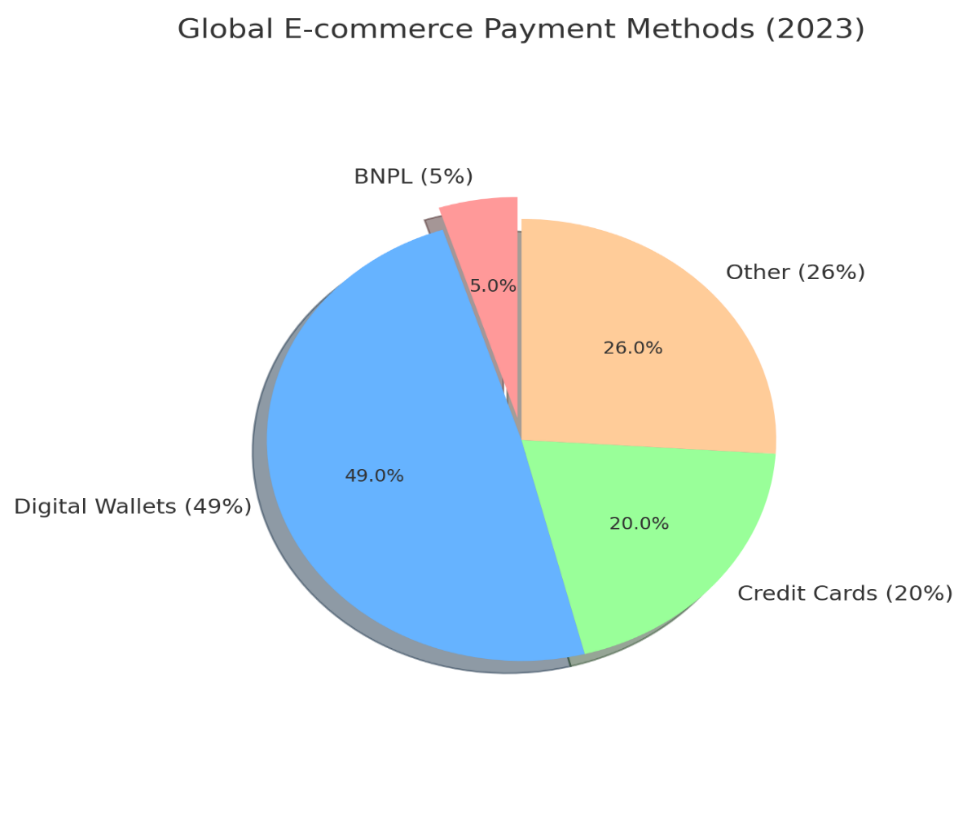

BNPL holds approximately 5% of global e-commerce transactions, compared to digital wallets at 49% and credit cards at 20% for e-commerce payments.

North America dominates the BNPL market, with a 30% share in 2023. The COVID-19 pandemic further accelerated its adoption, especially among Millennials and Gen Z consumers, who value financial flexibility.

Key players in the BNPL industry

Market leaders include:

Klarna: Dominates in Europe.

Afterpay: A strong player in the U.S. and Australia.

Affirm: Popular in North America.

PayPal: Offers “Pay in 4,” adopted by 57% of U.S. BNPL users.

Visa and Mastercard: Introduced their own BNPL solutions to stay competitive.

Customer segments and adoption rates

BNPL has especially resonated with younger demographics. In the U.S., 42% of adults aged 18 to 24 use BNPL, with the highest adoption seen among 25- to 44-year-olds around 50%. The service is particularly popular among women, who represent a larger share of frequent users, often purchasing clothing and fashion items. Overall, BNPL appeals to consumers with unmet credit needs or those wary of traditional credit card interest rates.

BNPL vs. Credit Cards: Market Dynamics

BNPL’s rise is gradually eating into the credit card market. Younger consumers, wary of high-interest rates, are increasingly favoring BNPL over credit cards, compelling credit card issuers to innovate to retain market share.

Leveraging analytics to strengthen BNPL

The Buy Now, Pay Later (BNPL) market is rapidly changing due to the shift in consumer behavior and other economic factors. To keep up, BNPL companies need to adapt data-driven solutions that help them manage risks, improve services, and stay resilient.

How can analytics address key challenges in BNPL?

Managing merchant risks

With the number of merchants facing financial pressure, BNPL providers must carefully select reliable partners. Using analytics, companies can evaluate a merchant’s financial health and market conditions. This helps identify and avoid high-risk partnerships, ensuring a stable and strong network of merchants.

Preventing consumer payment defaults

Economic uncertainty has made it more likely for consumers to miss payments. Credit risk analytics can help by assessing a customer’s ability to pay back, based on factors like past payment behavior and financial indicators. This way, BNPL companies can set safer credit limits and reduce the risk of defaults.

Improving customer engagement

Attracting and retaining customers requires a smart approach. Analytics can help by segmenting customers based on shopping and payment patterns. This lets BNPL companies create more targeted marketing and personalized experiences, building long-term loyalty and boosting customer satisfaction.

Better credit risk management

Analytics make it possible to automate and improve credit checks. By studying past and current data, BNPL platforms can set better credit limits and reduce the risk of financial losses. This keeps lending both responsible and profitable.

Stopping fraud early

Machine learning and data analysis are critical in catching fraud. By spotting unusual transaction patterns in real-time, BNPL providers can act quickly to stop fraud before it happens. This secures the platform and protects revenue.

Driving strategic growth

Data insights help BNPL companies find new ways to grow, like cross-selling or upselling products. By understanding customer preferences, companies can create personalized offerings that keep customers engaged. Feedback analysis and customer data ensure that services continue to improve and stay relevant.

Leveraging the analytics with advanced AI and cutting-edge tools businesses can enhance brand efforts and position themselves for growth in a rapidly changing landscape.

At LatentView, we harness the power of data and generative AI to solve BNPL challenges. Our approach includes credit risk modeling, fraud detection, and customer engagement strategies. By leveraging cloud technology and AI, we turn raw data into valuable insights, empowering BNPL companies to succeed in a fast-changing world.